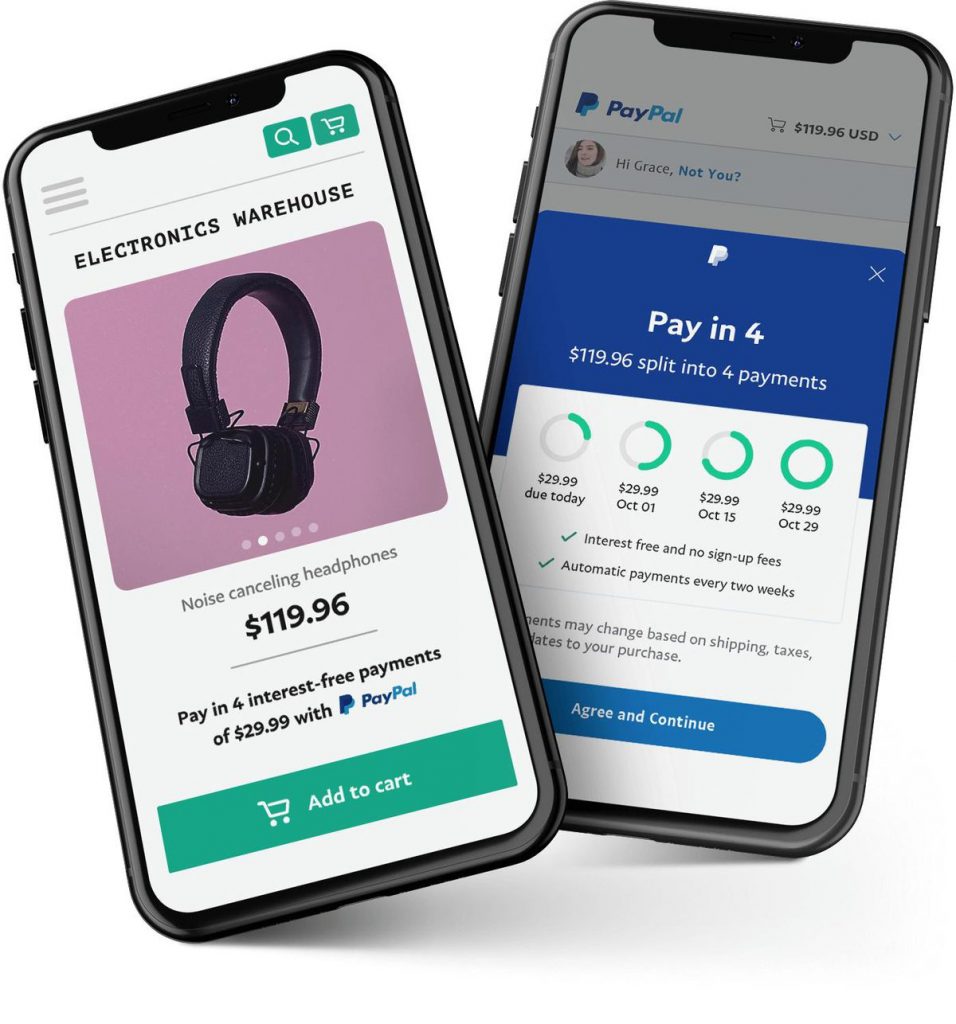

Point-of-sale financing – the modern item that allows you to pay for a new TV or dress in four installments instead of putting it on your credit card – has grown in popularity dramatically over the past two years, and the pandemic has propelled it to new heights. Australian company Afterpay, whose business is at stake in the program, has grown from a market valuation of $ 1 billion in 2018 to $ 18 billion today. Eight-year-old San Francisco-based startup Affirm is rumored to have an initial public offering of up to $ 10 billion. Now PayPal is entering the space. The new “Pay in 4” product will allow you to pay for any item that costs between $ 30 and $ 600 in four installments over six weeks.

Pay in 4 rates makes it different from other “buy now, pay later” products. Afterpay charges retailers approximately 5% of each transaction to provide its fundraising feature. It does not charge the consumer, but if a payment is late, they will pay a fee. Affirm also charges transaction fees to retailers. But most of the time, it forces users to pay 10-30% interest and no late fees. PayPal appears to be a less expensive hybrid of the two. You won’t charge consumer interest or additional fees to the retailer, but if you’re late on a payment, you’ll pay a fee of up to $ 10.

Serial entrepreneur Max Levchin started two of the top three players offering online point-of-sale financing in the USA. He co-founded PayPal with Peter Thiel in 1999 and started Affirm in 2012.

PayPal can hurt fee competition because it already has a dominant and highly profitable payment network that you can take advantage of. Eighty percent of the top 100 US retailers allow customers to pay with PayPal, and nearly 70 percent of US online shoppers have PayPal accounts. PayPal charges retailers a transaction fee of 2.9% plus $ 0.30, and in the second quarter, when Covid-19 shopped online like a rocket, it had a record $ 3 billion and profits of $ 1.5 billion. Its shares have exploded, adding $ 95 billion to market value in the past six months. In an economic environment where e-commerce is booming, “PayPal can grow 18% to 19% before waking up in the morning,” says Lisa Ellis, analyst at MoffettNathanson.

Data from Afterpay and PayPal shows that consumers spend more money, sometimes 20% more, when offered point-of-sale financing options. When PayPal launches Pay in 4 this fall, it will likely increase transaction size, and since they are already earning 2.9% on every transaction, the earnings will increase overall.

The online point-of-sale financing market has so far had millions of US customers. Afterpay, which expanded to the United States in 2018, has 5.6 million users. Affirm also says it has 5.6 million. Stockholm-based Klarna, 9 million, and Minneapolis-based Sezzle, has at least a million.

Separated from Pay in 4, PayPal has been providing point-of-sale financing for over a decade. They bought Baltimore start-up Bill Me Later in 2008 and renamed it PayPal Credit in 2014. PayPal Credit allows consumers to apply for a lump sum line of credit and today has millions of borrowers. Like a credit card, it charges high interest rates of around 25% and requires monthly payments. These consumer loans can present a high risk of default and PayPal does not hold most of them, transfers US loans to Synchrony Bank. (In 2018, Synchrony acquired PayPal’s extensive US consumer loan portfolio for approximately $ 7 billion.)

Last spring, as the pandemic spread rapidly and concerns about consumer defaults grew, PayPal halted lending. “Like many installment lenders, they basically stopped lending in March or early April” says Ellis of MoffettNathanson.

With Pay in 4, PayPal’s new credit boost indicates the business is becoming more aggressive in a volatile economy in which many consumers have performed better than expected so far. Unlike PayPal credit, PayPal will host these new loans on its own balance.

This article is shared by www.itechscripts.com | A leading resource of inspired clone scripts. It offers hundreds of popular scripts that are used by thousands of small and medium enterprises.